Compare the debt avalanche vs debt snowball method to find the best way to pay off your debt fast.

Last Updated: March 2026

If you’ve done any research on paying off debt, you’ve seen these two names come up constantly: the debt snowball and the debt avalanche. Both are structured repayment strategies that have helped millions of people eliminate debt. Both follow the same basic mechanic — pay minimums on everything, throw every extra dollar at one target debt, then roll that payment into the next. The difference is which debt you attack first. And that single difference has real consequences for how long you stay in debt, how much interest you pay, and whether you’ll actually stick with it.

How Each Strategy Works

Both methods start the same way: list all your debts, make the minimum payment on every one, and direct any extra money — even $50 or $100 a month — toward a single target. The difference is how you rank that target.

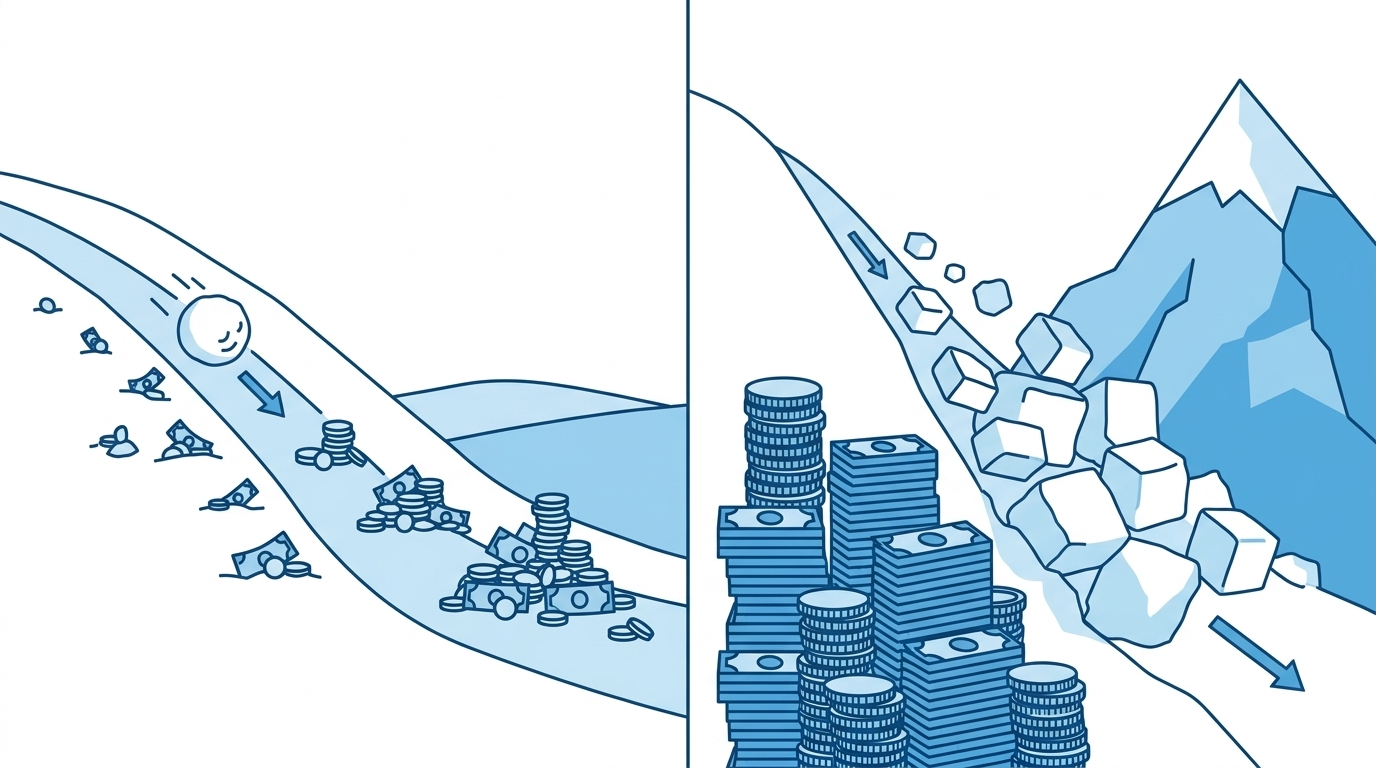

Debt Snowball: You order your debts from smallest balance to largest, ignoring interest rates entirely. You attack the smallest debt first with everything you’ve got. Once it’s gone, you take that entire payment and add it to the minimum you were already paying on the next smallest debt. Your payment gets bigger with each account you clear — like a snowball picking up mass as it rolls.

Debt Avalanche: You order your debts from highest interest rate to lowest, ignoring balance sizes. Your target is always the most expensive debt you’re carrying — the one costing you the most per day in interest. Once that’s gone, you move to the next highest rate. You’re dismantling your debts in order of how damaging they are to your finances.

In both cases, the momentum builds the same way: freed-up payments get stacked onto the next debt, accelerating payoff over time.

What the Difference Looks Like in Practice

Let’s say you have three debts and $300 per month to put toward them after minimums:

Card B: $4,500 balance — 24% APR — $90 minimum

Personal Loan: $8,000 balance — 11% APR — $150 minimum

Snowball order: Card A first (smallest balance), then Card B, then the loan.

Avalanche order: Card B first (highest rate at 24%), then Card A, then the loan.

With the snowball, you’d clear Card A in roughly 4 months — a fast, real win. With the avalanche, your first payoff (Card B) takes closer to 12–13 months because it’s a larger balance. But over the full payoff period, the avalanche method typically saves $1,000–$2,000 or more in interest on a debt load like this, depending on how long it takes.

The gap narrows when interest rates are close together. It widens dramatically when you have one card at 26% and others at 12% — in that case, the avalanche advantage is hard to ignore.

Side-by-Side Comparison

❄️ Debt Snowball

- Quick early wins boost motivation

- Easier to follow — just sort by balance

- Higher success rate for people who’ve quit before

- Fewer open accounts faster

- Pays more interest overall

- Takes slightly longer in most scenarios

🏔️ Debt Avalanche

- Saves the most money on interest

- Mathematically fastest payoff overall

- Directly attacks what’s costing you most

- Requires patience before first payoff

- Harder to stay motivated early on

- Best when rates vary widely

Why the “Best” Method Depends on You

On paper, the avalanche wins every time. It minimizes interest paid and — assuming you stick with it — gets you out of debt faster. But here’s the honest truth that most financial advice glosses over: a strategy you abandon at month four is worse than a slower strategy you follow through to month thirty.

Research on debt repayment behavior consistently shows that people who use the snowball method have higher completion rates. The psychological boost from eliminating an entire account — even a small one — triggers the kind of dopamine response that keeps people going. That momentum is real, and it matters.

The avalanche method, by contrast, can feel like you’re running on a treadmill for months. You’re putting extra money toward a $15,000 card at 24% and watching the balance drop from $15,000 to $14,600 to $14,200 — with no account closure in sight. For people who need visible milestones, that can lead to losing steam.

That said, if you’re analytical by nature, motivated by knowing you’re making the smartest financial decision, and patient with delayed gratification — the avalanche is the better choice. It’s not about which method is superior in the abstract. It’s about which one keeps you showing up every month.

How to Choose

Go with the Snowball if:

- You’ve tried to pay off debt before and lost motivation

- You have several small balances that can be cleared quickly

- Seeing a zero balance on an account is more motivating than saving money on paper

- You’re dealing with emotional stress around debt and need early wins to stay grounded

Go with the Avalanche if:

- You have one card with a significantly higher rate than the rest

- You’re disciplined and don’t need quick wins to stay on track

- The difference in interest savings between methods is large — thousands of dollars

- You’ve paid off debt before and know you can sustain effort without early milestones

Some people start with the snowball to build confidence, then switch to the avalanche once they have momentum. That’s not a compromise — it’s being strategic about what your actual situation requires.

📋 Quick Summary: Avalanche vs. Snowball

- Snowball: Smallest balance first — builds motivation through quick wins

- Avalanche: Highest interest rate first — saves the most money overall

- Both use the same mechanic: minimums on everything, extra cash on one target

- The interest savings gap is bigger when rates vary widely across your debts

- The best method is the one you’ll actually stick with for 12–36 months

- Starting snowball, then switching to avalanche is a valid strategy

🧮 See Your Payoff Plan in Numbers

Use our free tools to compare both methods with your real balances and interest rates.

Frequently Asked Questions

Q: Which is better, debt avalanche or debt snowball?

A: Debt avalanche saves more money in interest. Debt snowball builds motivation faster with quick wins. Both work — the best method is whichever you’ll stick to consistently.

Q: Can I switch between debt avalanche and snowball methods?

A: Yes. Many people start with the snowball to build momentum, then switch to the avalanche once they’re confident. The important thing is to keep making extra payments consistently.

Q: How long does it take to pay off debt using these methods?

A: It depends on your total balance, interest rates, and how much extra you pay each month. Use our Debt Payoff Calculator to get a personalized estimate based on your actual numbers.

Financial Disclaimer: The content on this page is for informational and educational purposes only. It does not constitute financial, legal, or credit advice. DebtToolbox is not a financial advisor. Always consult a qualified financial professional before making decisions about your debt or finances.